Matt Taibbi Misexplains Crypto: Part 1

Dissecting "Return of the Great American Bubble Machine"

In what is becoming a regular encounter with Gell-Mann amnesia for me, this is the second piece about one of my favorite writers misunderstanding things. The first one discussed how Matt Taibbi misexplained hedge funds and other financial topics to Joe Rogan during a podcast discussion earlier this year. And here I am again to highlight confusion Mr. Taibbi recently demonstrated while writing about crypto.

He wrote two pieces on the topic: One that focuses on concerns regarding Circle - issuer of the popular stablecoin USDC - and another that talks about how crypto’s purportedly failed effort at decentralization makes it just another “great American bubble machine”.

These are both topics worthy of discussion. But I found Mr. Taibbi’s treatment of them to be lacking and ultimately demonstrative of the limitations of journalistic tourism (i.e., when a non-expert attempts to understand complex topics and reports on conclusions derived from superficial knowledge).

By way of disclaimer, I don’t consider myself an expert when it comes to crypto, which may seem counterintuitive. However, I’ve invested in several parts of the ecosystem so am dangerous enough when it comes to knowing how it actually works. I am not technically proficient in the underlying technology but I understand very well how the space trades. When it comes to crypto, speculation is the primary use case for me. While I’m by no means a diehard on the asset class, I remain openminded about its potential. I therefore suffer maximalists and denialists alike.

What I’m more interested in is accuracy in reporting. And even with my admittedly moderate knowledge of crypto, I found multiple instances of misunderstanding with Mr. Taibbi’s posts on the topic.

Since this became way too long for a single post, I’m splitting it into two parts that treat each of his pieces individually. We’ll start by taking on the one entitled “Return of the Great American Bubble Machine”.

Mr. Taibbi led the bubble piece by marveling at the amount of wealth destruction that has occurred within the digital asset market in recent months. He framed the devastation by noting an “astonishing” $700 billion in losses from early May through June. This is a pet peeve of mine because absolute numbers don’t mean much without context. I mean, sure, $700 billion sounds like an awful lot. But it pales in comparison to the trillions in stock market losses incurred during the same period. A more effective way of describing the abysmal performance of an asset is to state its total rate of return. In the case of crypto, being down in the neighborhood of 65% on the year would’ve been descriptive enough, which of course could be punctuated by total dollar amounts.

He then highlighted the collapse of algorithmic stablecoin TerraUSD (UST) as a key triggering event of the crypto selloff. At roughly $20 billion in market capitalization, UST had grown to become one of the largest stablecoins and underpinned a broader ecosystem that was bursting with promise. The collapse of UST - which basically involved loss of its 1:1 peg with the U.S. dollar (USD) - revealed a massive web of leverage and cross-collateralization that took down a number of major industry players. More on this later.

Mr. Taibbi attributed further “market mayhem” to a disclosure that Coinbase made in a regulatory filing which seemingly suggested that customer assets could be confiscated in the event of the company’s bankruptcy.

$200 billion vanished from the valuation of crypto companies within 24 hours as, among other things, the share price of Bitcoin, the leading crypto product, fell on the news.

This is an oddly worded sentence for anyone familiar with markets in general and the crypto one in particular. Putting aside the strange use of the term “valuation” in this context, Mr. Taibbi appears to be confusing traditional finance (TradFi) and decentralized finance (DeFi) concepts.

By referring to companies, one might assume he means publicly-listed crypto entities like Coinbase (COIN), Galaxy Digital (BRPHF), RIOT Blockchain (RIOT), etc. But that cannot be the case since the combined market capitalization of these companies peaked at roughly $100 billion last year.

He must therefore be referring to the total value (not valuation) that was shed across the entire crypto asset class, which includes the thousands of coins and tokens comprising the ecosystem. This would indeed appear to be the case since, per CoinGecko, the total market capitalization of crypto declined approximately $165 billion from end-of-day May 10 to end-of-day May 11.

But to refer to all those coins and tokens as companies is misplaced. These are not companies issuing shares of equity on a stock exchange. They are instead projects and protocols with tokens attached to them. These tokens aim to - among other things - facilitate usage, promote uptake and accrue value to holders. In some cases, these digital assets attempt to perform the function of a currency (as with bitcoin) but most of them offer some other utility.

For example, FTT is the native token for the popular FTX exchange. Holders of FTT receive various perks like discounted trading fees on the FTX platform. But FTT is no more a company than individual shares of Apple stock represent companies in and of themselves.

Also, there is no “share price” of bitcoin as there are no shares in any related company to be purchased. Bitcoin simply trades at a price relative to a reference asset and is most often nominally quoted in U.S. dollar (USD) terms. It’s the same way one does not buy shares of euros; they instead just buy euros.

And conventional definitions of bitcoin consider it to be some combination of commodity and currency, so referring to it as a “product” feels strange, especially since there is no central organizing entity producing and distributing it. Are copper or the USD ever described as such?

Lastly, a semantic note: The capitalized spelling of Bitcoin refers to the network. The lower case spelling of bitcoin refers to the cryptocurrency (BTC).

More importantly, Mr. Taibbi incorrectly suggested that one event was the cause of another. The reality is that Coinbase’s disclosure had little to do with crypto performance in the days surrounding it. In fact, BTC (a good barometer for general price action) was actually up about 3% on the day of the Coinbase news. Also up on the day was the Nasdaq Composite Index, which advanced about 1%. BTC did fall (-6%) the day following the announcement, but so too did the Nasdaq (-3%).

Generally speaking, crypto price action this year is more a function of broader macro dynamics than idiosyncratic developments within the industry (one exception being the Terra debacle and resultant carnage). As many have long observed, crypto has been the beneficiary of easy monetary policy for most of its existence. And now that the U.S. Federal Reserve has embarked upon an aggressive rate hiking cycle, the era of easy money is coming to an end. This has resulted in a massive repricing of all risk assets. It’s therefore no surprise that crypto’s correlation with the Nasdaq has spiked these past several months. And as a beta play on growth, we typically see crypto shadow the Nasdaq in punchier fashion.

In tying crypto price action to that Coinbase disclosure, Mr. Taibbi not only tried to force a false narrative but also revealed his own naivete on the subject. Putting aside the low probability of a Coinbase bankruptcy in the near term - and whether user coins would actually be at risk anyway - most crypto users understand very well the risks associated with keeping their coins on exchange. There’s a popular saying within the community that nicely captures this sentiment: Not your keys, not your coins. This effectively means that those choosing to entrust custody of their crypto assets to a third party - like an exchange - are knowingly sacrificing some degree of ownership and control in the process.

So if anyone actually grew concerned about the viability of Coinbase, their (rational) instinct would not be to sell everything but instead to simply move their coins to another exchange or - better yet - to a self-custodied wallet. The latter is something that Coinbase itself has encouraged, having rolled out its own self-custody wallet called Coinbase Wallet. A self-custody wallet transfers ownership of one’s private keys to that wallet, leaving its contents beyond the reach of any third-party entity.

Coinbase volumes did spike in the days surrounding the disclosure but remained well below historical highs. And there was another event occurring around the same time - the de-pegging of UST - which may explain at least some of the heightened activity.

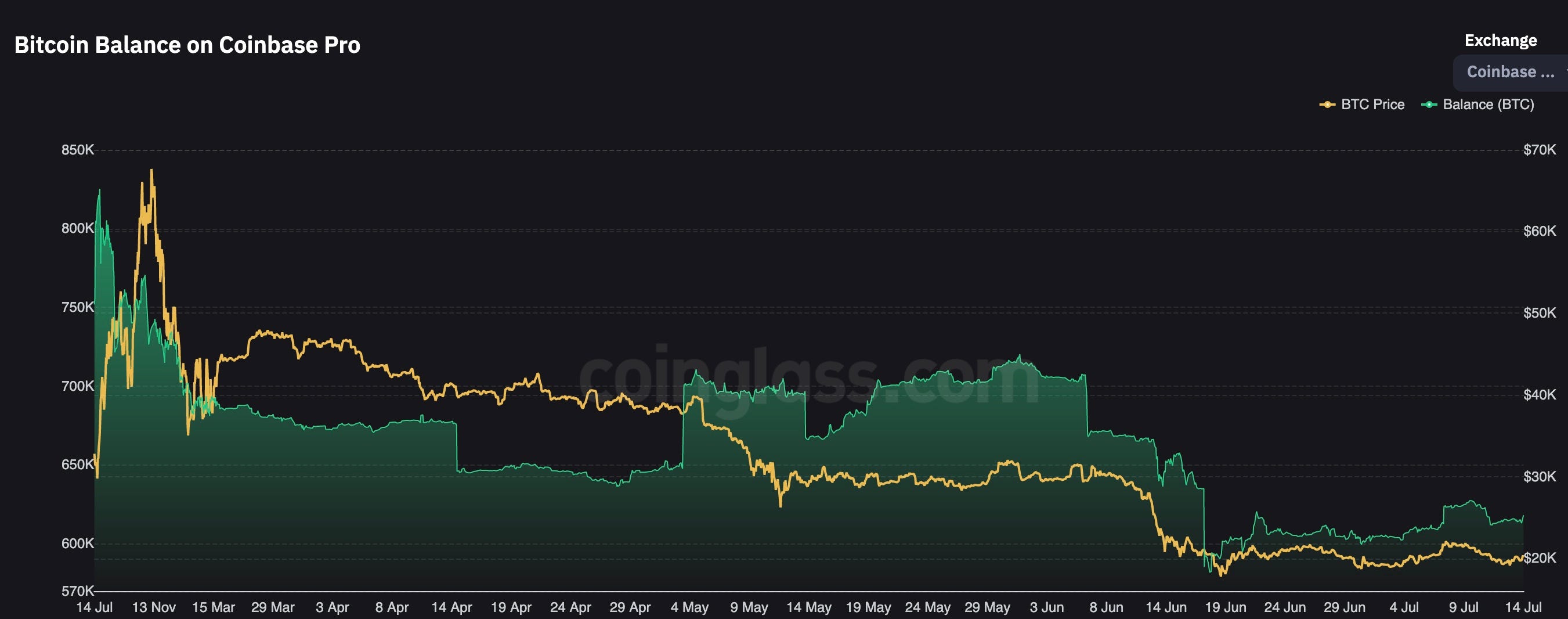

Interestingly, the bitcoin balance on Coinbase was relatively steady during the days surrounding its disclosure, suggesting investors weren’t particularly concerned about it. A bigger dip came later on May 13 as the demise of UST progressed.

Source: Coinglass.

The fact is that coins have been fleeing exchanges for a while now. This used to indicate intention to hold crypto for the long term (noting coins moving back to exchange typically portends sell pressure). But wariness of counterparty risk is undoubtedly playing an increasing role.

This gets to what I perceive to be the heart of these two pieces for Mr. Taibbi. My guess is that he looked around at all the madness playing out in cryptoland and began to pattern match by looking for historical corollaries. What he saw was a fledgling industry succumbing to many of the same problems of the very industry it seeks to disrupt. Coinbase could go bankrupt and take its customers coins with it? Some groups basically operated as illiquid, leveraged hedge funds that could become insolvent? And one of the biggest stablecoin projects could lose its peg and a bunch of money for its users in the process? What is decentralized and better about any of this?

There is merit to this argument and it speaks to a longstanding tension within the crypto community between CeFi and DeFi entities. The problem though is that crypto appears to form a synecdoche in Mr. Taibbi’s mind whereas it is instead comprised of wildly disparate but interconnected parts.

Crypto purists eschew all manner of CeFi as best they can. But the reality is that some CeFi elements are required in order for the system to function. For example, exchanges like Coinbase and FTX are centralized entities. Though they ostensibly exist to facilitate things like DeFi, they nonetheless operate in conflict with crypto’s core operating ethos that espouses decentralization. But in order to make an initial purchase of crypto, one typically needs to have fiat (USD, EUR, JPY, etc.) on hand to do so. These exchanges are the only fiat on/offramps available to most crypto users, which forces engagement with these centralized entities at entry and exit.

Once a user converts their fiat to BTC, ETH, USDC, etc. on exchange, they are free to take their crypto and traverse the growing landscape of DeFi outside of the exchange. But if they ever want to take liquidity along the way, they’ll be required to return to a centralized exchange and convert their crypto back into fiat for transfer to their TradFi bank account.

So centralized exchanges act as a necessary evil for much of the crypto community. There are of course decentralized exchanges that populate the world of DeFi. But they require possession of other coins in order to transact, which takes us back to the initial requirement to use centralized exchanges as onramps.

Less necessary are shadow banking businesses like Celsius, BlockFi, Voyager Digital and Vauld, groups forming the epicenter of today’s crypto storm and sharing similarities with the leveraged asset-liability mismatch machines that characterized the GFC. These are each CeFi entities that take deposits from customers looking to earn yield on their crypto holdings and use those deposits to earn excess yield of their own. They do this through extending loans to other crypto entities, yield farming and proprietary trading (among other things).

There have been other culprits too, including the now infamous hedge fund Three Arrows Capital (TAC). The fund reportedly had $18 billion in assets under management at its peak but was recently forced into liquidation thanks to the souring of a number of leveraged bets.

As witnessed over the past few months, this is all a dangerous game to play in crypto. The nature of the digital asset class reminds me of the geopolitical acronym VUCA: Volatility, Uncertainty, Complexity, Ambiguity. Simmering under the surface of an already volatile space was a mountain of self-contained but illiquid debt that left the space on a razor’s edge. So when UST collapsed and took the broader Terra ecosystem down with it, a cascade of margin calls and forced liquidations was triggered. Related selling directly impacted crypto prices and also influenced a lot of selling among those looking to front-run the forced unwind. This created a vicious cycle of selling that saw June become the worst month in history in terms of crypto price action.

To hear Mr. Taibbi tell it, this all means that crypto has failed as just another American bubble. Two things here.

First, bubbles routinely inflate and deflate in crypto. BTC has experienced peak-to-trough drawdowns of 50%+ at least half a dozen times before, so this sort of price action is par for the course.

Second, Mr. Taibbi conflates notions of transparency and governance within blockchain technology itself with these various CeFi entities causing all the trouble. Outside of the Terra debacle, most crypto projects have been operating just fine amidst all the stress. Bitcoin continues to churn out block-after-block and DeFi performed admirably despite the adversity. Transparency may have gone to die with some of these CeFi entities but it remains standard operating procedure within most native projects themselves.

Importantly, these CeFi entities cannot entirely escape the forced transparency of the blockchain that Mr. Taibbi thinks has been betrayed. This is because they all have wallets attached to them whose transactions are easily traceable. For example, we can watch in real time as Celsius reclaims collateral from DeFi lending platforms in order to buttress its liquidity position.

So it’s not so much that crypto has failed at its objective as it’s been bastardized by groups looking to capitalize on the industry’s growth. Mr. Taibbi’s claim is a little like saying mortgages failed because the GFC happened. The problem obviously wasn’t the concept of mortgages. Sure, there were plenty of mortgages that were poorly structured, just like there are plenty of crypto projects guilty of the same. But it was largely the repackaging and securitization of mortgages by investment banks that led to the whole mess. We’ve seen a similar dynamic play out in cryptoland with centralized entities developing their own witches’ brews of complexity. But just as mortgages continue to perform a legitimate function, so too does the underlying technology of blockchain.

Mr. Taibbi spent the rest of the bubble piece drawing parallels between the shenanigans seen in TradFi during the 2008 Global Financial Crisis (GFC) and what is taking place today in cryptoland. In doing so, he made a number of questionable claims.

Firstly, pointing to increased lobbying efforts by the industry as evidence of it “buying all the questions” is disingenuous to me. As a nascent industry that has grown from nothing to several trillion dollars in just over a decade, it stands to reason that it would mature in its political savviness along the way. And a lot of the activity thus far has involved certain industry leaders testifying before Congress via Q&A sessions designed to educate America’s political class on a topic about which they know very little.

The fact of the matter is that most of crypto’s CeFi players welcome regulation. The more clarity there is on this front, the more comfortable large traditional players will feel to engage with the space. The hope, of course, is that any regulation is of the “smart” variety, hence the desire for certain actors to grow more engaged with the powers that be.

As the saying goes: don’t hate the player, hate the game.

Second was this quote:

On January 3, 2009, an anonymous computer developer going by the name Satoshi Nakamoto created the first “Bitcoin,” a form of digitized currency designed as a technological solution to the problems posed by companies like Lehman Brothers. In fact, the “genesis block” of Bitcoin, i.e. the first-ever unique unit of digital currency…

Bitcoin’s genesis block was not “the first-ever unique unit of digital currency”. That first block instead formed the foundation of the immutable database that became the Bitcoin blockchain. Blocks are basically discrete data sets of recorded transactions on a network. The information contained within is verified by a process called mining, which is a computationally intensive effort to guess a random number. Miners are incentivized with rewards for correctly solving that number. The rewards associated with mining that genesis block came in the form of the very first bitcoin (50 to be exact). So to correct Mr. Taibbi, that first block was not itself the first unit of digital currency; rather, it precipitated the issuance of those first bitcoins as a reward.

Third was this quote:

Even the ultimate symbols of upper-class financial respectability, the auction houses Sotheby’s and Christies, got in on the act. These companies, whose very names imply frumpy establishment legitimacy, not only began accepting cryptocurrency as payment for properties like an untitled $5.4 million Keith Haring painting, but held auctions for NFTs, or non-fungible tokens, a kind of digital currency that at the time was having success as a speculative investment.

An NFT is not a kind of digital currency. The reason for this is in the name: non-fungible. This means each NFT is unique. Conversely, fungibility is a critical feature of any currency. For example, one BTC can be exchanged for one BTC in a transaction of equals, just like one $10 bill can be exchanged for another $10 bill. The entire point of NFTs is that they are not fungible and instead represent ownership of a singular, unique thing. So it would be better to refer to NFTs as a digital asset rather than a digital currency.

Fourth was this quote:

Wells Fargo and Chase launched Bitcoin funds in August of 2021, while both the NASDAQ and the NYSE began listing crypto-based exchange-traded funds, and in yet another stone cold repeat of 2008, pension funds began plunging their money into crypto properties, with the Houston firefighters’ fund in October of 2021 being among the first.

Mr. Taibbi’s mention of the NASDAQ and NYSE listing crypto-based ETFs requires some explanation. U.S. regulators have yet to approve a “physically-backed” crypto ETF despite repeated efforts by industry to get one to market. The reluctance of regulators to approve a bitcoin spot ETF has in fact contributed to some of the problems plaguing the space today, namely involving the travails of the Grayscale Bitcoin Trust. There are a handful of ETFs that trade bitcoin futures but none of them are allowed to hold crypto directly. The biggest related ETFs are instead those investing in stocks of companies active in blockchain or crypto. So the ETFs Mr. Taibbi is referencing here would be better described as crypto-related rather than crypto-based.

And assuming by “properties” he means “investments”, Mr. Taibbi makes it sound like there’s been a rush into digital assets among U.S. pension funds. But I’ve only heard of a small handful allocating to the space. In addition to Houston firefighters, a couple of Fairfax county pensions allocated to a crypto venture capital fund as well as a crypto hedge fund. But that’s pretty much it. And these allocations have been tiny. Houston firefighters invested 0.5% of its pension directly in BTC and ETH while the Fairfax allocations amounted to about 1.7% of combined pension assets. The reality is that pensions are only just beginning to explore the space and are far from “plunging” into it.

Lastly, looking at crypto as a “great American bubble” isn’t quite right. While some of the problem children of this latest cycle are U.S.-based, crypto is very much a global phenomenon. The largest crypto exchange in the world by a country mile, Binance, is based in Malta by way of China. Terra was headquartered in South Korea. TAC was relocating to Dubai by way of Singapore. And as Sam Bankman-Fried (SBF) has testified before Congress, 95% of all crypto trading occurs offshore. (SBF is the founder of FTX, itself based in the Bahamas by way of Hong Kong).

A primary reason for this is the generally antagonistic treatment of crypto by U.S. regulators. So instead of Mr. Taibbi’s assertion that crypto has been allowed to run rampant because of acquiescent regulators and politicians, the U.S. is actually an inhospitable jurisdiction for digital assets. This might be the result of concerted efforts by regulators to protect a legacy financial system by squelching innovation, or it could derive from a genuine desire to look after retail investors.

I reckon it’s more a function of an ossified regulatory bureaucracy that doesn’t know how to deal with the birthing of an entirely new asset class. Similar to how the FBI and CIA didn’t know how to talk to each other prior to 9/11, confusion reigns amongst the SEC, CFTC, etc. in understanding exactly what should be done to bring oversight to a space as dynamic and confusing as crypto.

I’ll soon be publishing part two of this post, which focuses on Mr. Taibbi’s run at stablecoin issuer Circle.