More Cowbell & The Paranoid Style of FinTwit

The market has a fever, the cure for which is apparently more cowbell.

There’s a classic Saturday Night Live skit that stars Will Ferrell, Horatio Sands, Jimmy Fallon, Chris Parnell and Chris Kattan as members of Blue Oyster Cult. The sketch features the band working on its hit song (Don’t Fear) the Reaper with music producer Bruce Dickinson, played by the incomparable Christopher Walken.

Entitled More Cowbell, the segment elevates Ferrell’s cowbell to a hilariously annoying centerpiece of the song, with Walken comically pleading for “more cowbell” throughout. The theatrics of Ferrell’s cowbell grow with each take as both he and the instrument eventually dominate the proceedings.

The phrase “more cowbell” has come to mean different things in pop culture. For me, it analogizes an engagement strategy often seen on Financial Twitter (FinTwit), which involves promulgating all manner of fear porn in order to harness paranoia for clicks.

The analogy thusly works as follows: the cowbell is the fear porn; Will Ferrell’s character represents social media personalities propagating that fear; the rest of the band is everyone else engaged in normal discourse; and Christopher Walken’s character is the FinTwitdiot crowd pining for more doomer content.

We all know fear sells. Appealing to it is an effective form of marketing for many businesses (and religions). Fear forms the bedrock of the insurance, gun, pharmaceutical, defense, and security industries, to name just a few. Turn on your local evening news and the headline story will surely be a horrific accident, violent act or some other misdeed. Cable news outlets thrive on fear and division, just like the politicians who grace their airwaves.

A similar sort of doomer echo chamber has emerged on FinTwit. Many of the most popular accounts tend to feature variations on common doomsday themes. These doomers play on the paranoid style that Richard Hofstadter eloquently wrote about when describing the nature of American politics:

It is the use of paranoid modes of expression by more or less normal people that makes the phenomenon significant…no other word adequately evokes the sense of heated exaggeration, suspiciousness, and conspiratorial fantasy.

Research shows that negative content is three times more likely to be clicked than the positive variety. The reason this happens is because we’ve been hardwired for such entrancement dating back to our caveman days. The psychological concept that underpins the modern version of this is called negativity bias, which:

refers to the fact that humans focus on negative events, information, or emotions more than their positive counterparts. In more dangerous times, this bias may have provided an evolutionary benefit (e.g., we were more likely to notice potential threats to our safety). But in the modern world, our preference for the negative has been harnessed to keep our attention.

This helps explain why the news consistently emphasizes stories on the worst things happening in the world, both on the global (wars) and the local levels (robberies). So not only are we seeking out the negative, but media outlets are actively trying to give us more of it. It’s a double dose.

FinTwit is well-suited to capitalize on this phenomenon since the subject matter is inherently complex. This evokes a related concept called negative differentiation, which states that:

since negative events are by nature more complicated than their positive counterparts, we require a more significant mobilization of cognitive resources to minimize the consequences of the event and deal with the experience, making it a more memorable and intense experience.

Combine this negativity dynamic with good storytelling and you’ve got a powerful formula for FinTwit success. Accuracy has little bearing on whether someone can achieve popularity as a FintTwit bear, for the cowbell exists more for entertainment than as a source of wisdom. As Hofstadter noted, “style has more to do with the way in which ideas are believed than with the truth or falsity of their content.”

This speaks nicely to the appeal of the FinTwit doomsayer. These gurus regularly hold court on Twitter to push a narrative that our financial world is collapsing. They sound smart and savvily play to emotions as they weave stories that make logical sense to minds attracted to negative complexity. And because the listener can connect the dots, they get to enjoy the endorphins that come with understanding.

This helps explain the doomer idolatry that has fueled the popularity of untold numbers of FinTwit personalities. Cursory reviews of the most popular accounts will find them littered with gloomy projections. The titles of their Spaces discussions are usually some derivative of “Everything is Fucked”. Even Substack sweetheart Doomberg has doom in their name.

A Washington Post OpEd on the topic of fear has a quote apropos the moment:

What distinguishes the present age is the widespread and lucrative focus on the apocalyptic: the magnification of threats and minimizing of opportunities; the exaggeration of differences; the desire to see things as worse than they are. We invent ever-more-outlandish conspiracies, impute ever-baser motives, foretell ever-bleaker futures.

There is of course nothing fundamentally wrong with being bearish, at least episodically so. Bear markets occur with some frequency and of course should be discussed. The problem arises when bearishness is ever-present and comes to define one’s persona - aka the permabear - or when one completely loses their shit anytime an actual bear market rolls around. Of particular concern is when one’s supposed bearishness - however temporary or permanent - is exploited for clicks.

Let’s review some examples.

The quintessential permabear is also one of the most infamous ones, Peter Schiff. While correct in warning against risks that gave way to the Global Financial Crisis (GFC), the man has been wrong about almost everything else since. Same with contemporaries such as Nouriel Roubini, a professor turned pundit who also came to fame for his supposed prescient calls around the GFC. He too has been dead wrong about most things ever since but that hasn’t dented his media popularity. As it turns out, Roubini has a new book coming out called Megathreats, which sounds like an uplifting read.

Schiff’s fund management capabilities can best be described as mediocre and he has become a laughingstock across the internet for how consistently wrong he has been. Yet he lives on as a FinTwit favorite with over 800,000 followers. He’s done this by incessantly preaching about the impending death of the U.S. dollar and collapse of the global financial system along with it. Everything is a bubble according to Schiff, except of course gold, which he’s been championing since the start. Examples of his wrongness would easily fill this page. I instead encourage readers to simply Google “Peter Schiff wrong” and enjoy the show.

Notwithstanding his clownishness, Schiff’s media playbook has proven a successful one, at least in terms of notoriety. He’s constantly featured as a foil on podcasts, including ones as big as Joe Rogan. And a whole cottage industry of doomer copycats has followed in his wake.

Someone else who did well in the GFC but hasn’t done much since is Michael Burry, he of The Big Short fame. Fittingly named Cassandra on Twitter, reading his feed is a study in pessimism. Everything sucks everywhere all the time. He predicted a global financial meltdown and the onset of WWIII in 2017 (he may finally be proven correct this year!). His on again, off again relationship with Twitter has him neurotic about his tweets. But an archival account goes back to 2020 to give us a flavor for his particular style of bear porn. Burry has 1.1 million followers lining up to consume his steady stream of cowbell.

Marc Faber is the grizzled veteran doomer, a thoughtful man whose monthly commentary makes for interesting (and sometimes controversial) reading. But with an earned nickname like Dr. Doom as author of his Gloom, Boom and Doom Report, one can easily discern the tone of his missives. A simple Google search will return a lot of headlines like this one:

The enduring appeal of these doomers is curious given their track records, which brings to mind a recent tweet that captured well this phenomenon:

The sentiment expressed here is spot on. But it equally applies to those who manage capital, as evidenced by Schiff and others.

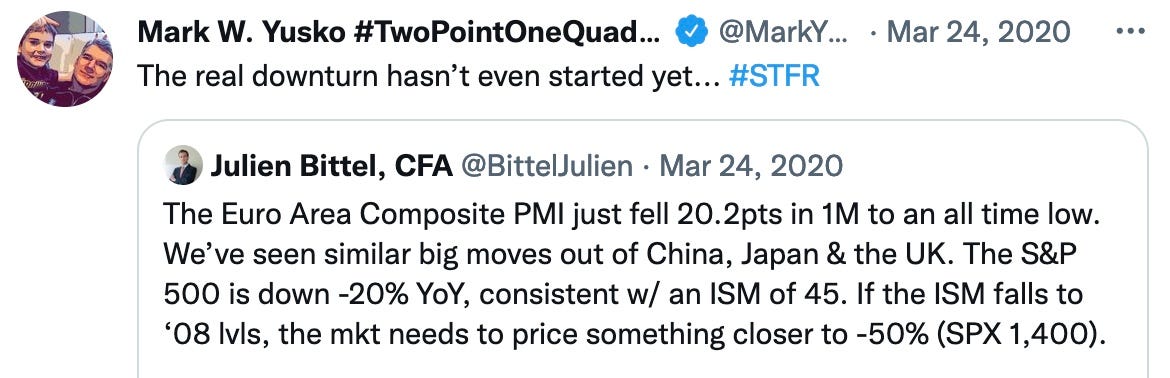

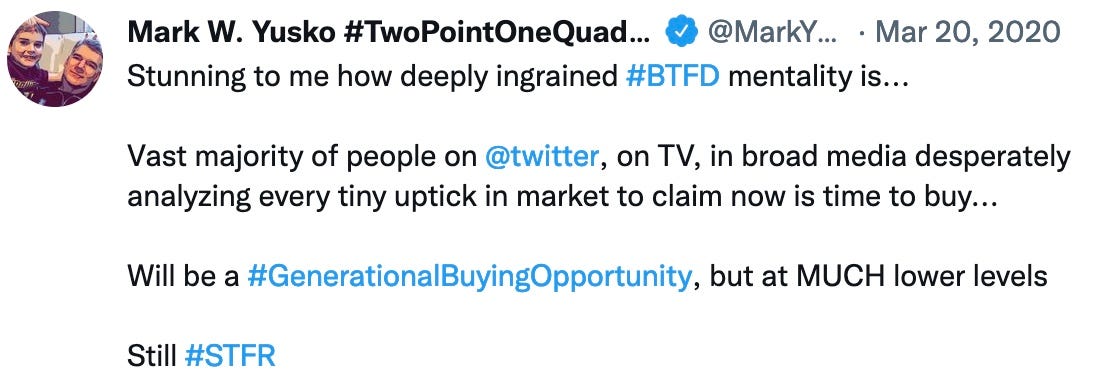

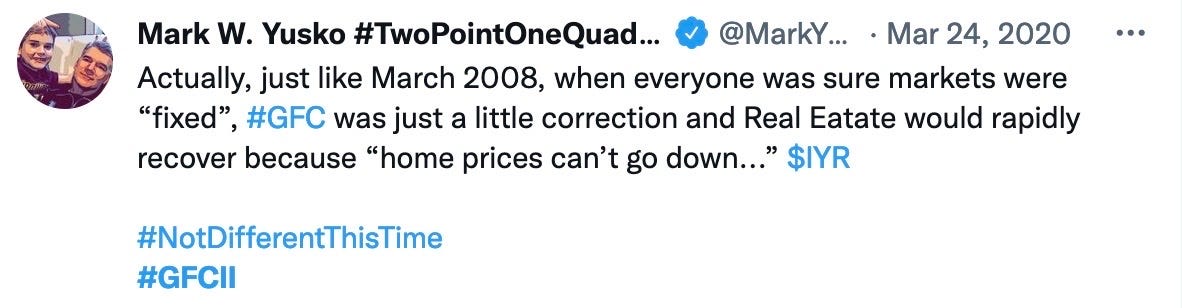

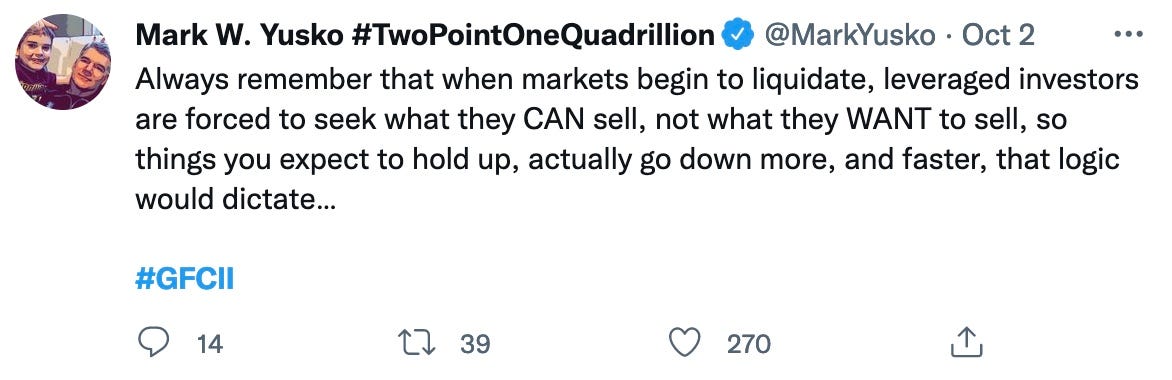

For example, there are nervous nellies like Mark Yusko, the loquacious founder of Morgan Creek Capital Management and former partner of disgraced crypto promoter, Anthony Pompliano. Yusko resembles a permabear in so far that his bitcoin maximalism has him seeing central bankers as the sum of all evil. But his ultimate sin lies in his overreactive bear state. This is a man who manages billions of dollars yet was busy warning us about a “GFCII” during the COVID selloff while also suggesting that we “STFR” (sell the fucking rip) literally at the market lows.

And here he is now warning yet again about a GFCII amidst another bear market:

Here’s what I’d be looking for from a money manager in times of stress: A calm, level-headed assessment regarding the current state of play and what opportunities may be presenting. I would not be looking for someone prone to hyperbole on Twitter. Whether his theatrics are calibrated for attention or because he is pissing down his leg in real life, the shame applies either way. Nonetheless, Yusko enjoys a Twitter following of nearly 150,000 and is a mainstay on the conference speaking circuit.

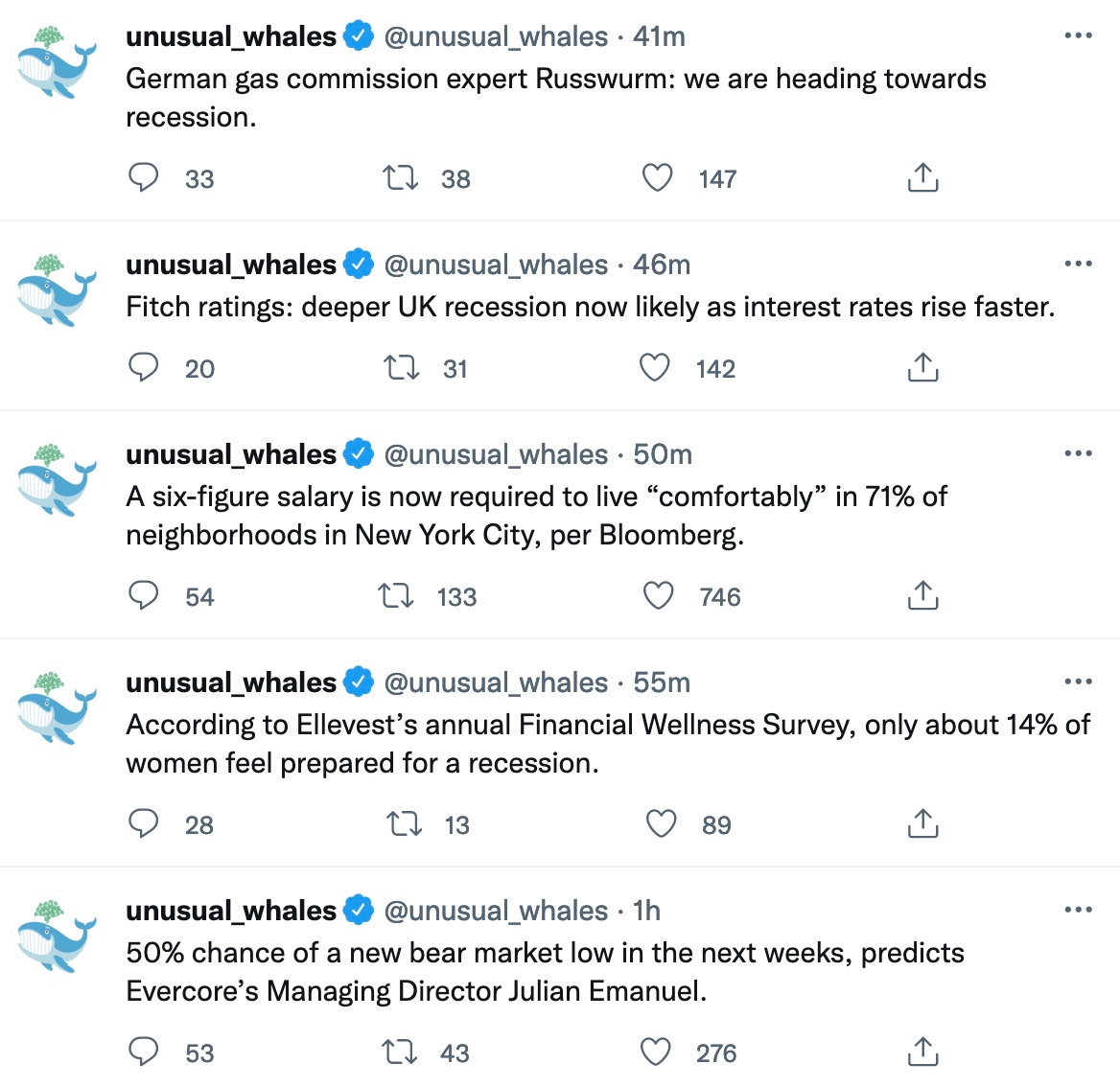

Unusual Whales (UW) is a good example of the bad news bear who disingenuously mines fear and bias for clicks. With over 800,000 followers, this account is among the most manipulative on FinTwit. Evidence for this lies in the superficiality of its options reporting and in the constant misrepresentation of congressional trading data. I suspect UW understands well the calculus involved to maximize attention while doing its best short-form Zerohedge impression. This can be seen in a casual review of its Twitter feed, where negative headlines outweigh the positive ones by at least 5:1. A selection from yesterday’s feed provides a good example:

The grand papa bear these days is infamous stock-picker turned FinTwit ragelord and ETF day trader, George Noble. With the temperament of an aging wombat, it’s easy to imagine his emotional bear state. Noble’s bearishness has proven correct this year, which he’s happily flaunted on his way to social media stardom - which in turn has been parlayed into an ETF launch. Combined with his cantankerous demeanor and the regular bear orgies that he hosts on his Spaces, Noble is among the more entertaining and outspoken doomers of this cycle. True to form, his newly-launched NOPE ETF was initially structured as an end-of-the-world portfolio that was long gold/Treasuries and short growth.

What’s striking about Noble and his bear ilk is the masochism they display when cheering for something to break. He believes the underbrush built up over years of monetary excess needs to be cleared, collateral damage be damned. He has “no sympathy for anyone who loses money being long in this market”, tossing aside the millions of pensioners and average buy-and-hold retail investors who would be crushed by any systemic collapse through no fault of their own. When the inhumanity of such a stance was pointed out on a recent Spaces, Noble of course went apoplectic on the brave guest who dared to challenge his thinking.

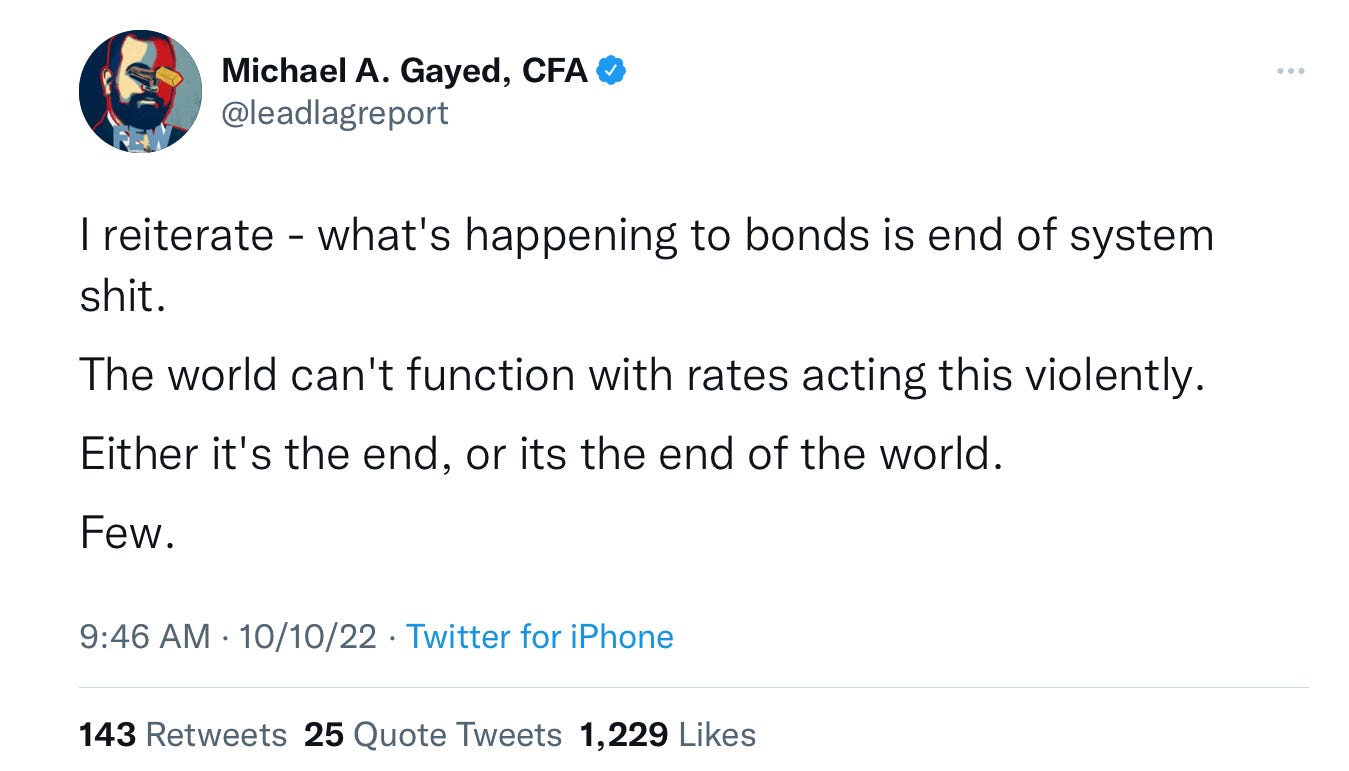

The hyperactive bear is best exemplified by Michael Gayed, publisher of the Lead-Lag Report and portfolio manager of the ATAC fund family. He has built a nice following on the back of his own brand of bear porn to go along with a constant stream of written and verbal content. A good example of his fearmongering is his go-to marketing tweet, which appeals directly to the fear of loss among investors.

Ironically, his funds are getting killed this year thanks to the naivete of applying a static, rules-based approach to complex, dynamic markets. The ATAC funds are based on models that reference the historical behavior of various assets to form a risk-on/risk-off approach theoretically designed to weather all markets. Notwithstanding the mediocre performance of his strategies prior 2022, this year has been particularly difficult with his funds down 30-50%.

Gayed is naturally perplexed by what is happening today and is greeting that confusion with cowbell tears. Rather than acknowledge the limitations of backtesting, he continues to worship at its alter and begs understanding while constantly whining about the anomalous nature of today’s market. And instead of doing what every successful quant in history has done - which is continuously refine and adapt their models - Gayed claims slave to the prospectus while employing the Norman Dale approach to systematic investing.

As an aside, it’s pretty funny how enamored Gayed is with backtesting. He’s claimed that “you don’t know a damn thing about what’s real and what’s not” if you haven’t done a backtest. And he’s actually tweeted the following generic insult to anyone who questions his bearishness - “Bro - you’ve never done a single backtest and you’re 16 STFU” - which may qualify as the nerdiest imaginary takedown of all time.

Watching Gayed self-immolate in front of his 700,000 followers is fascinating. The man appears to be in the midst of a nervous breakdown and is airing it for the world to see. In his explanation of things, the financial world is collapsing because the behavior of risk assets doesn’t make sense to him. It’s not his models at fault, it’s the market to blame. At least that’s what he spends most of his time telling his followers these days. Instead of acknowledging the reality of stock-bond correlations, he’d rather scare the bejeezus out of everyone by suggesting the end of the world is nigh.

The following interview gives us a glimpse of the hyperactive bear in peak form.

What Gayed says here is patently absurd. It’s fear porn at its finest. He’s literally suggesting that America is at risk of anarchy and despotism because Treasuries are not performing the way he expects. This is obviously ridiculous. But he looks serious when saying it so we must take him seriously.

In actuality, Gayed is Taleb’s Intellectual Yet Idiot come to life. He’s the academico-investor who just can’t comprehend that models work until they don’t. He gets “the first order logic right but not second-order (or higher) effects, making him totally incompetent in complex domains.” This has been an expensive lesson for him to learn as his funds are estimated to have vaporized ~$100 million of investor capital this year.

Gayed’s example joins with that of Schiff’s to remind everyone that sounding smart on Twitter is entirely different from being a moneymaker in real life. Unfortunately, many on FinTwit conflate the two, or look past implementation and go straight to the prognostication. I suppose popularity has become a business model for these characters in the same way that Paris Hilton is famous for being famous.

Speaking of idiots, what got me thinking about all this was a recent introduction to the work of Chris Irons, a podcaster and blogger who publishes under the name Quoth the Raven.

Irons is a sort of self-fashioned, everyman pundit. His formative experience has been described as growing up in a household with low bullshit tolerance that espoused living within one’s means. He loves telling the story about how he is a former bartender who stumbled his way into the investing world, first through teaching himself how to trade then as an analyst at micro-cap specialist, GeoInvesting. He also had a random stint as the head of investor relations for a company that was eventually found the be fraudulent.

Irons has no formal training in economics or finance but that hasn’t stopped him from waxing philosophical on these topics. He seems to have met with some success in doing so, garnering over 200,000 followers on Twitter and enough Substack subscriptions to quit his day job.

He appears to have gotten his writing start over at Seeking Alpha, where he would provide penetrating insight like the below:

This is one of the great things about the internet. Democratization of content creation, distribution and consumption allows folks like Irons to build an audience with armchair takes on investing, just like it allows a technology product manager to build a strong following by fashioning himself a macro expert. And here I am, an amateur writer attempting to…write.

Irons is a Schiff fanboy who came to FinTwit fame doing his best mini-me impersonation of his hero. Like his idol, the gist of Irons’ world view is that the government and associated organizing bodies basically suck at everything. This is especially true when it comes to monetary policy and most things macroeconomics. The aforementioned OpEd has a quote that sums up nicely Irons’ general take: “Our problems are too large for our leaders, who are too small for their jobs.”

Philosophically, Irons places himself squarely in the Austrian school of economics and rarely misses an opportunity to shit on his Keynesian counterparts, especially those of the MMT variety. Naturally, he wrote a piece about how MMT is destroying America.

Irreverence seems to be Irons’ defining feature. He’s positioned himself as an average bloke with normal friends who likes to drink beer and often swears and oh yeah check out his cool tattoos. He’s kind of like the Barstool Sports version of Schiff, so I guess it sounds cooler when he tells us everything sucks.

I was introduced to Irons’ work through a piece that he made free to everyone entitled “A Broken Clock Cries Wolf Twice A Day”. A disastrous collection of mixed metaphors, it was just too important to stay behind his paywall. The post is basically a high school essay about how Keynesianism sucks and what a shame it is that its proponents “think they have it all figured out.” The implication here is that Irons and his Austrian friends are the ones who have it all figured out, an irony clearly lost on the author.

Irons goes on to feature all types of fear porn in the piece, the most comical of which involves Russia and China exploring their own (gold-backed?!) reserve currency to challenge the U.S. dollar. This is a ridiculous concern to anyone familiar with how geopolitics and foreign exchange markets work in real life. But it’s kind of cute to see Irons reveal his rudimentary understanding of things while warning against a “shit sandwich the likes of which this country has never seen before.”

I could continue ad nauseam about how silly his piece is but instead encourage readers to give it a look themselves. A review of his other free pieces as well as his Twitter feed will reveal similar levels of comedy.

Just as Maajid Nawaz sprung from the bowels of extremist ideology and now peddles insane conspiracy theories, Irons was born of fraud and now sees it everywhere. He holds authority in deep contempt and has a special distaste for experts and their academic jargon. He’s managed to channel that spite into a nice little niche for himself but that doesn’t mean he has the slightest clue what he’s talking about.

For me, Irons is the FinTwit equivalent of comedian Dane Cook. I was always amazed at how the latter achieved such extraordinary success despite lacking any semblance of insight or humor in his standup. I’m equally amazed at how Irons has managed to build an audience for analysis that is as unoriginal as it is vapid. The man simply regurgitates Austrian school tropes with a dash of conspiratorial nonsense to boot. His writing is as tortured as his thinking, both in content as well as style. His output is the literary and audible equivalent of wasted calories. Yet his popularity persists thanks to the enormous amount of cowbell he pushes out.

The below speech provides a good sense for the man’s style and overall take on things:

What stood out to me here was how uninteresting his speech was, how so proud of himself he was for giving it and how immature he behaved. I’m not one to stand on formality. But for fuck’s sake if George Noble invited me to give the keynote at NOPE’s investor conference next year - to celebrate his triumph over the haters, of course - I’d have the decency to at least wear pants. Instead, Irons is just so fucking cool that he strolls into a professional investment conference wearing a tank top, shorts and flip-flops while sipping a beer to regale us with such remarkable thoughts as, “If you have something where the supply is limited, it retains its value, for the most part.” Oh and look at his sweet tattoos.

We were also treated to more of his standard tone deafness in this speech: “We don’t know where this unprecedented experiment in monetary policy is going to go…Anybody that tells you that they know exactly where this whole thing is going…That’s really the most arrogant thing you can do in finance.”

Alas, he knows where it’s all going. And he’s here to write and make speeches about it.

The zero fucks given schtick appears to be working for him, as disingenuous as the act might be. For someone who flippantly claims he doesn’t care if anyone reads his Substack, he seems awfully happy to advertise subscription discounts, conduct frequent giveaways and encourage people to subscribe to his various outlets otherwise. He also often claims that he doesn’t want to go on anyone’s podcasts yet routinely pops up on them to enlighten us with his meandering streams of consciousness (he’s the press play and listen kind of guest).

I do find it funny how he gets away with making fun of the suits in this speech. It’s kind of like how Robin DiAngelo, controversial author of White Fragility, gets paid to tell a room of white people that they’re all inherently racist. I can just imagine how many times Irons pulled this video clip while showing off to his buddies at the bar how awesome he is because he just doesn’t give a fuck.

Speaking of DiAngelo, a review of her book can be paraphrased to describe Irons:

[Irons] does not offer profound insight into [markets]. Rather, [his bear porn] is religion masquerading as knowledge. [Irons’] conception of [Austrian economics] isn’t hard won wisdom. It’s an unprovable and unfalsifiable theory, deceptively framed to convince readers of their own guilt. [Irons] relies on rhetorical tricks and skewed interpretations of ambiguous events to deceive readers, in the same way a zealot tries to gain converts.

Irons gave another breathless speech on gold at the Kase Learning conference in 2018, during which he made fun of analysts and economists for being wrong all the time. The speech was terrible for plenty of other reasons (e.g., less is more when it comes to words on a slide), but the hypocrisy was just another level for me. Similar to Schiff, it’s too easy to point out all the ways that Irons himself has been wrong. But suffice to say it happens a lot, especially when it comes to his obsession with gold, which has annualized at a whopping 2.5% over the past decade.

Irons puts on a show of self-deprecation but I call bullshit. His disclaimer is cleverly worded to point out that he’s wrong all the time. He says the same thing on his various podcast appearances. It reminds me of how Jon Stewart used to hide behind the cloak of comedy whenever challenged on his political commentary. Just like we’re not supposed to take Stewart seriously because he’s a comedian, nor should we take Irons seriously because he calls himself an idiot.

But that betrays the seriousness with which he obviously takes himself through his writing and speaking. He’s trying to have it both ways here, which may work on some but certainly not on all of us.

By way of disclaimer, I have no special love for Keynesians myself. I grew up in the Chicago school and have read plenty of Mises, Rothbard and Hayek. I actually sympathize with a lot of the views our doomer friends have. I just have no patience for the way they go about propagating them.

And to be fair, there are permabulls that are equally egregious in their commentary and approach. Tom Lee of FundStrat is one that springs to mind and I’m sure there are many more. And I tend to agree that Keynesian cheerleaders like Paul Krugman have become caricatures of a different sort.

But being bearish all the time is not only a bore but also unproductive. It’s like a basketball player who only shoots half-court shots. Sure, you’ll nail a shot here and there that’ll be met with oohs and ahhs, but you’ll annoy the shit out of your teammates and fall afoul of all analytics in the process. Similarly, these doomers will be right on occasion and I suppose right at the very end. As Keynes famously said, “In the long run, we are all dead.” But the average run of markets will find these bears consistently on the wrong side of reality.

The fact is that bear markets happen all the time. There have now been 27 of them since 1929, averaging one every 3.5 years. Bear markets tend to last about 10 months and bring average declines of approximately 35%. It could be that this time is different and that the permabears are finally vindicated amidst a paradigm-shifting meltdown of epic proportion. It could be that all those panic bears are finally justified in their hysteria as the system indeed resets.

Or it could be that this is just another bear market and we recover from this one just as we’ve done the 26 prior ones. The long-term march of our species is one of progress just like the long-term trend of markets is upward. Which reminds me of a little investing secret that I often share: The greatest macro trade of all time is betting against the end of the world.

I reckon there are only three ways to combat the FinTwit doomsayer.

Ignore them, though admittedly hard to do in the way that it’s difficult to avert one’s eyes from a train wreck.

Respond to their tweets with the following GIF:

Reply to their posts with this coopted response: “OK doomer”.

Yours in pragmatism,

FTJM

I appreciate the overall point of this article, that some people overdo it with the negativity. But I have been listening to Chris's QTR podcast for years and I get a lot of value from it. The mainstream orthodoxy seems to be that all you have to do is just put all your money in a stock index fund and trust the market to take care of you. I used to believe this until I discovered Chris (and others that one might call "permabears"). Sometimes I follow discussions among Mustachians and FIRE enthusiasts; they obsess over the exact details of withdrawal rates in retirement, and just take it as a given that the stock market will go up. You can quibble with Chris's style if you want, but still I think it remains true that he provides a valuable counterpoint to the mainstream just-put-everything-in-an-index-fund perspective.

I also wonder what exactly you think Chris has gotten wrong. As far as I can remember, he has not been predicting imminent market collapses or anything like that. (Except perhaps in early 2020, when he was right!) His overall point is that there are fragilities in the markets that we should be aware of, even though we can't know exactly when the problems will manifest themselves. Chris was also right in a huge way in predicting that covid would be a big deal, back when the official narrative was that it was "just the flu."

Let me ask you this: if you don't like Chris Irons then who would you recommend instead? Because I think there are definitely important and valuable things he talks about that are hard to find in the mainstream.

Good read. One thing I would say about Marc Faber is that he may be cantankerous and disdainful of politicians and central bankers, but he stays invested; he is not a “world is going to end go to cash/gold” type of guy. He focuses on diversification and doesn’t push risky strategies like some of the other doomers (short selling etc)